How profitability, embedded finance, and AI are redefining the region’s fintech trajectory

Not long ago, fintech was the brash insurgent – long on ambition, short on profits, and determined to unseat incumbents at any cost. Today, it is no longer circling the banking system; it is embedded within it. It is also closing on half a trillion dollars in revenue. This new phase is more structured. Investors are now prioritizing profitability and sustainable growth.

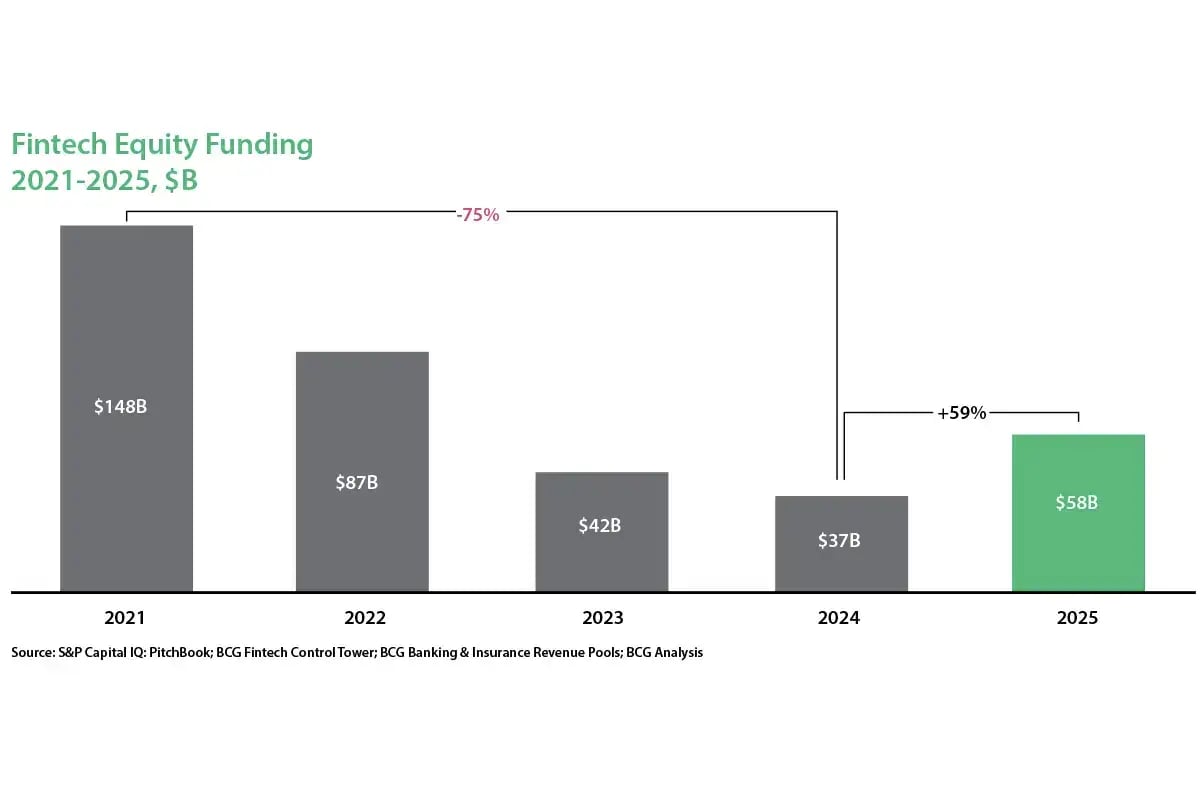

The funding slowdown of 2021–2024 (equity funding fell about 75 percent from 2021 to 2024) reset pricing expectations and reinforced selectivity. However, it also strengthened the region’s leading platforms. Many of these now command premium valuations on the back of scale, regulatory alignment and improving margins.

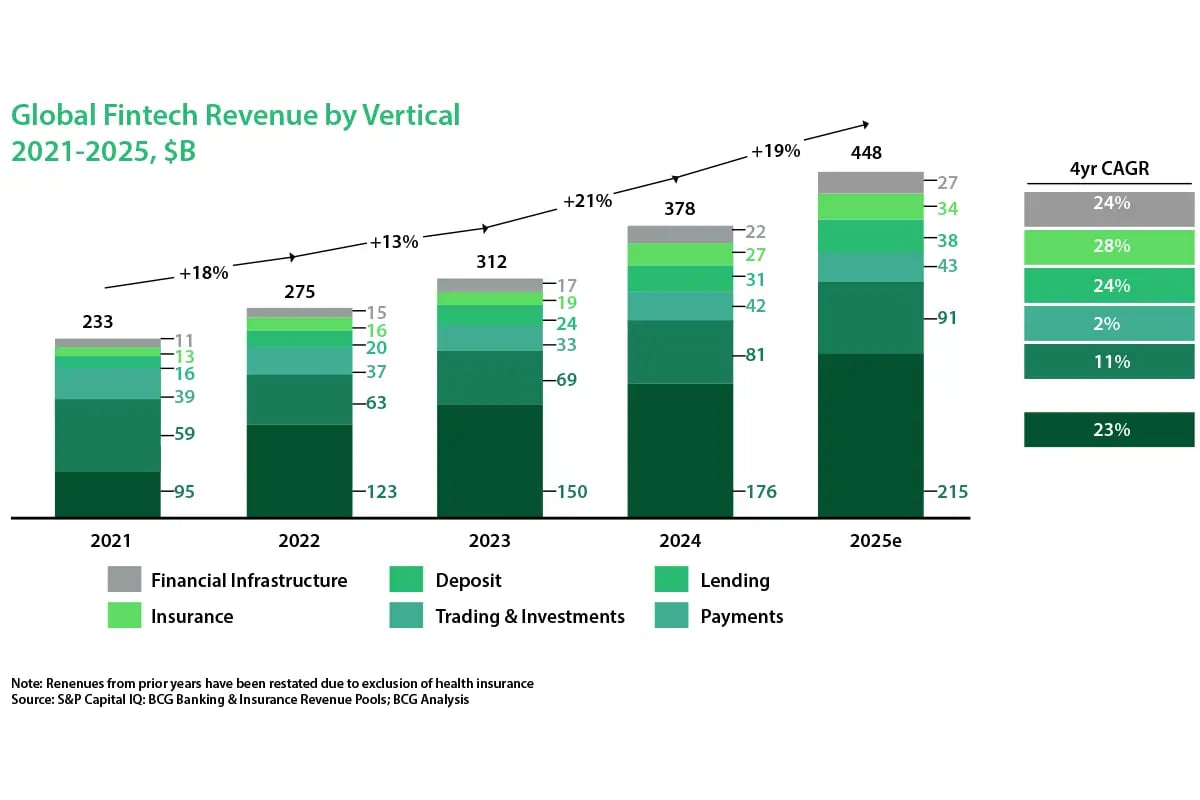

Fintech revenues have grown about 14 percent per year over this period and about 20 percent in 2024 and 2025. Moreover, around 70 percent of public fintech are now profitable Digital payments underpin global commerce. Lending platforms shape credit access for households and SMEs. Wealthtech democratizes investing, and B2B infrastructure quietly powers everything from cross-border settlement to compliance.

Embedded finance has turned retailers and marketplaces into financial distributors. As a result, it has unlocked revenue pools once reserved for banks.

Having survived funding winters and regulatory scrutiny, the sector is trading rapid scaling for durability and cash flow. With artificial intelligence redefining productivity and onchain finance hinting at programmable markets, fintech stands at a new threshold – less rebellion, more reinvention.

From reset to resurgence

In the GCC, fintech funding has evolved from early-stage momentum into a more mature and diversified capital story. The early part of the decade was marked by rapid acceleration. Increasingly larger venture rounds began backing payments, BNPL and digital banking platforms.

By 2023–24, the ecosystem experienced a natural pause that reset valuations and shifted investor focus toward unit economics, governance and sustainable growth rather than pure customer acquisition.

In 2025, the trajectory has turned upward again. Saudi Arabia and the UAE have both reported materially stronger funding activity compared to the subdued 2023–24 period. Deal counts are rising and later-stage capital is returning to the market.

This renewed momentum has helped cement a growing roster of regional fintech unicorns, particularly in BNPL and payments, with several platforms reaching multi-billion-dollar valuations and positioning themselves for potential public listings over the coming years.

Crucially, capital is now flowing toward models with clearer paths to profitability — payments infrastructure, embedded finance, open-banking enablers and regulated digital banks. At the same time, the underlying revenue pools continue to expand. Electronic payments penetration rises and SME and consumer credit digitizes.

Together, these dynamics suggest that GCC fintech funding is entering a more durable phase —one underpinned not just by optimism, but by scale, improving economics and structurally growing revenue opportunities.

Growth is moving closer to the customer

This new generation of regional fintech is quietly unlocking revenue pools that incumbents long overlooked. Their edge lies not only in strategy, but in structure:. Lean operating models, cloud-native infrastructure, and nimble technology stacks allow fintech to launch, iterate, and scale products at a fraction of the cost and complexity borne by traditional banks.

By contrast, many incumbents remain constrained by layered processes and legacy IT systems. This makes rapid innovation difficult and expensive.

The most powerful shift is embedded finance. Rather than asking customers to visit a bank, fintech are inserting payments, lending, and insurance directly into digital journeys — at e-commerce checkouts, on mobility apps, and within B2B marketplaces.

In the GCC, embedded finance is projected to grow from a niche segment worth a few hundred million dollars in the early 2020s to a multibillion-dollar opportunity by 2030. Merchant-funded buy-now-pay-later (BNPL) models in the UAE and Saudi Arabia illustrate the shift. Instead of relying solely on interest margins, providers monetize point-of-sale conversion uplift and data-driven underwriting.

Open banking is widening the aperture further. Regulators are enabling secure data sharing and fostering ecosystems where fintech can build budgeting tools, alternative credit models, and SME financing solutions on top of bank infrastructure. This allows them to capture fee income and customer relationships banks historically underpenetrated.

The result is not merely competition, but redefinition: Revenue once considered peripheral is becoming central to the Gulf’s next era of banking growth.

A measured march to market

Against this backdrop, valuations have settled into a more disciplined groove — less momentum-driven, more metrics-anchored. The IPO conversation has become increasingly tangible.

Regional exchanges in Saudi Arabia and the UAE remain broadly supportive, and bankers point to a measured pipeline for 2026–2028. In BNPL, Tabby and Tamara are widely viewed as frontrunners should market conditions cooperate.

In payments, Network International and fast-growing acquirers such as Hala and Geidea, sit in the frame as consolidation and scale sharpen equity stories.

Infrastructure players like Lean Technologies and Tarabut are building the open-finance rails that could underpin future listings. Meanwhile, digital banks including Wio, STC Bank and D360 represent another cohort of potential candidates as they mature their deposit bases and lending books. The likely outcome is not a flood of flotations, but a selective procession.

The next chapter: Smarter, programmable finance

If the first act of fintech was about putting financial services online, the next may be about letting them think, and move on their own. Agentic AI is still early, largely confined to copilots in engineering, compliance, and customer support. However, its trajectory is clear: From assisting decisions to executing them.

Over time, financial agents could monitor cash flows, rebalance portfolios, optimize payments, and even renegotiate credit, quietly reshaping economics built on inertia and manual intervention.

At the same time, onchain finance is inching from experiment toward infrastructure. Stablecoins are gaining relevance in cross-border corridors, but the larger prize lies in tokenized assets that reduce settlement friction, unlock liquidity, and compress intermediary costs. Should tokenization reach critical mass, payments and collateral could follow natively onchain, creating a programmable financial stack.

The convergence of autonomous AI agents and programmable assets would not merely digitize finance — it would rewire it. The question for leaders today is not whether change is coming, but whether their institutions will shape this new system — or be shaped by it.

Hesham Elmais is the Managing Director and Partner at Boston Consulting Group.